What is Gross Profit Margin?

Gross Profit Margin is the amount of money you make on selling a good or service before you deduct overheads. For example, if you bought a product for $60 and sold it for $100, the $40 then is your gross profit. This equates to a gross profit margin of 40/100 = 40%.

The aim in business is always to achieve a maximum or high gross profit margin. The higher the gross profit, the more money the business has to cover overhead expenses.

It is important to track your gross profit as it shows the profitability and financial performance of a business. Simply put, if the costs of goods (COG) increase, the gross profit decrease and vice versa. The same can be said for decreasing and increasing the sales price of an item.

Net Profit vs. Gross Profit

As mentioned before, gross profit refers to the profit made after subtracting the costs associated with the manufacturing and selling of the product or service. Net profit margin, on the other hand, is the amount of money your business retains after deducting all operating, interest and tax expenses.

Going back to the example earlier, if you’ve sold 100 items with a gross margin of $40 each, your total gross margin is $4,000. Now, if your other fixed costs (rent, wages, insurance, etc.) amount to a total of $3,000, your net profit is then $1000.

How to calculate gross profit margin?

Net sales – Cost of goods sold = Gross Profit Margin

Net sales – This is the revenue or total amount generated from the sales of the product or service for a period of time.

Costs of goods sold – These are the direct costs used for producing the product or service. This includes the costs of labour and materials.

Ways to Increase Gross Profit Margin

Be strategic about your pricing

Pricing plays a significant role in increasing your gross profit margin. You need to set prices that accurately value your products and services.

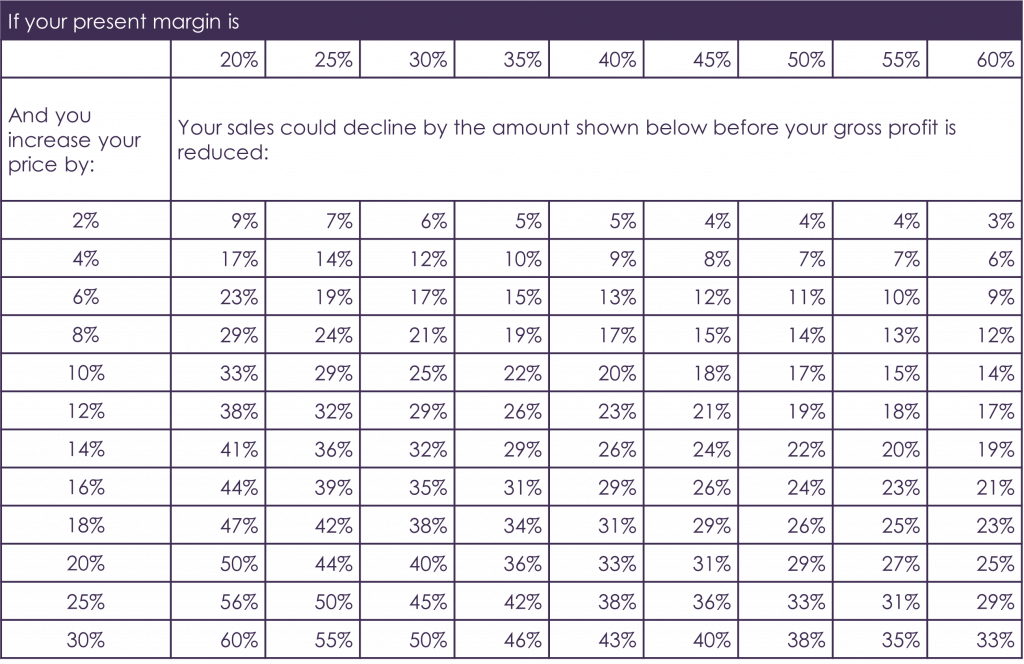

Increasing your prices without increasing the cost of goods is a good way to boost your margins and improve your bottom line. This tactic can be tricky though, as it can mean losing customers to cheaper competitors. However, if the decline in sales volume can be offset by the total revenue caused by the price increase, then that more than justifies the increase.

This is demonstrated by the table below:

You can also justify the price increase by adding value to your products or providing a better customer experience. According to research, 86% of buyers are willing to pay more for a better customer experience. Not all customers base their purchasing decision on pricing so it’s best to study your target market and take all things into consideration before setting a price.

Strengthen Supplier Relationships

No business operates entirely on its own– many businesses use suppliers or third-party companies to help them with products or other functions. As a business owner, it’s important that you develop a good working relationship with your suppliers. After all, as your business grows, your supplier’s business grows too.

It’s more cost-efficient to streamline your product lines and get them all from one vendor. You can even ask your supplier for a discount on goods you buy in bulk so you can decrease the cost of goods and, in turn, maximise your gross margin.

Increase sales by retaining customers and promoting to new ones

Making your products and services more attractive to customers can greatly help increase sales and get a higher profit margin. It’s crucial that you have good branding and marketing strategies in place to promote your product and gain new customers.

That said, the focus should not only be on generating new customers– retaining existing customers and encouraging brand loyalty can greatly help your business. In fact, a study by Bain and Company found that increasing customer retention by 5% can increase revenue by 25-95%. Not to mention, it’s actually more affordable to retain an existing customer than to acquire a new one.

Reduce Operating Expenses

As you go along in your business, you can start to assess areas you can do without and, therefore, save more money. Review all your business expenses personally and try to find areas of wastage. These can be little things that add up to a whole lot of additional expenses.

One way to do this is to look at your inventory and see if you are ordering or producing more goods than necessary. If you have a surplus of a certain item just sitting in your backroom, maybe it’s time to think about reducing production or phasing the product out totally.

Wastage can also come from your manpower. Are you leveraging your team’s skills and potential? Or do some employees do the wrong tasks? Take a look at all the business components individually and think of ways to eliminate or reduce unnecessary expenses.

Get expert business advice from Craig Allen & Associates

Craig Allen and Associates is a CPA practice that aims to work with businesses in building a strong financial platform, ensuring good record-keeping, improving their tax result and increasing their profitability. We are experts in helping small businesses grow by providing expert business advice.

Schedule a free, no-obligation consultation now by contacting our team at 039 558 7316 or emailing us at craig@craigallen.com.au.

SHARE THIS ARTICLE